Why talk of a housing bubble is blowing up

Talk of a housing bubble is beginning to crop up as home prices continue to appreciate at a rapid pace this year. Well, not so fast! Although the appreciation of residential real estate is well above historic annual averages, there are other factors to consider.

First, let’s look at the numbers:

According to the Federal Housing Finance Agency (FHFA), annual appreciation since 1991 has averaged 3.8%.

2020 appreciation percentages range somewhere in the 7% range, nearly double the average annual appreciation:

- FHFA: 7.8%

- CoreLogic: 7.3%

- Case-Shiller: 7%

Everything about 2020 has been odd and all-in-all, one thing has led to another to leave us with such high appreciation numbers. And, really, as a homeowner, I’m not complaining one little bit! Let’s put these numbers into context before we talk bubble.

Scarcity and affordability were a problem before 2020 but, the major life changes of 2020 added significantly to the tightening of residential home sales. Many buyers report expediting their home search timeline during the pandemic, citing low interest rates and the potential to get a good deal on a home as their main motivation. While ‘getting a deal’ was a rarity due to scarcity in our inventory, there were more motivating reasons that became priority.

A vast majority (74%) of those speeding up the process are repeat buyers. Active buyers are moving due to major lifestyle changes (I.E. homeschooling & working from home) and according to Forbes, the following are the biggest reasons:

- Extra bedrooms (43.5%)

- Open floor plan (45.7%)

- Good lighting (45.7%)

- Kitchen style (50%)

As remote work continues to be the ‘norm,’ two criteria that previously ranked very important to many buyers – location and commute times – are no longer a priority. Instead, buyers are now able to focus on neighborhoods, communities, suburbia and lifestyle. The work-from-home phenomenon is enabling more buyers to live where they want to live. Buyers now want home offices, gyms, and flex rooms that are suited for private video conferencing, away from other household members.

Barbara Ballinger, a freelance writer and the author of several books on real estate, recently wrote:

“While homeowners continue to want their outdoor spaces that offer a safe retreat, that appeal has shifted into other parts of the home, coupling comfort with function. In other words, homeowners want amenities for work and leisure, and they plan to enjoy them long after the pandemic.”

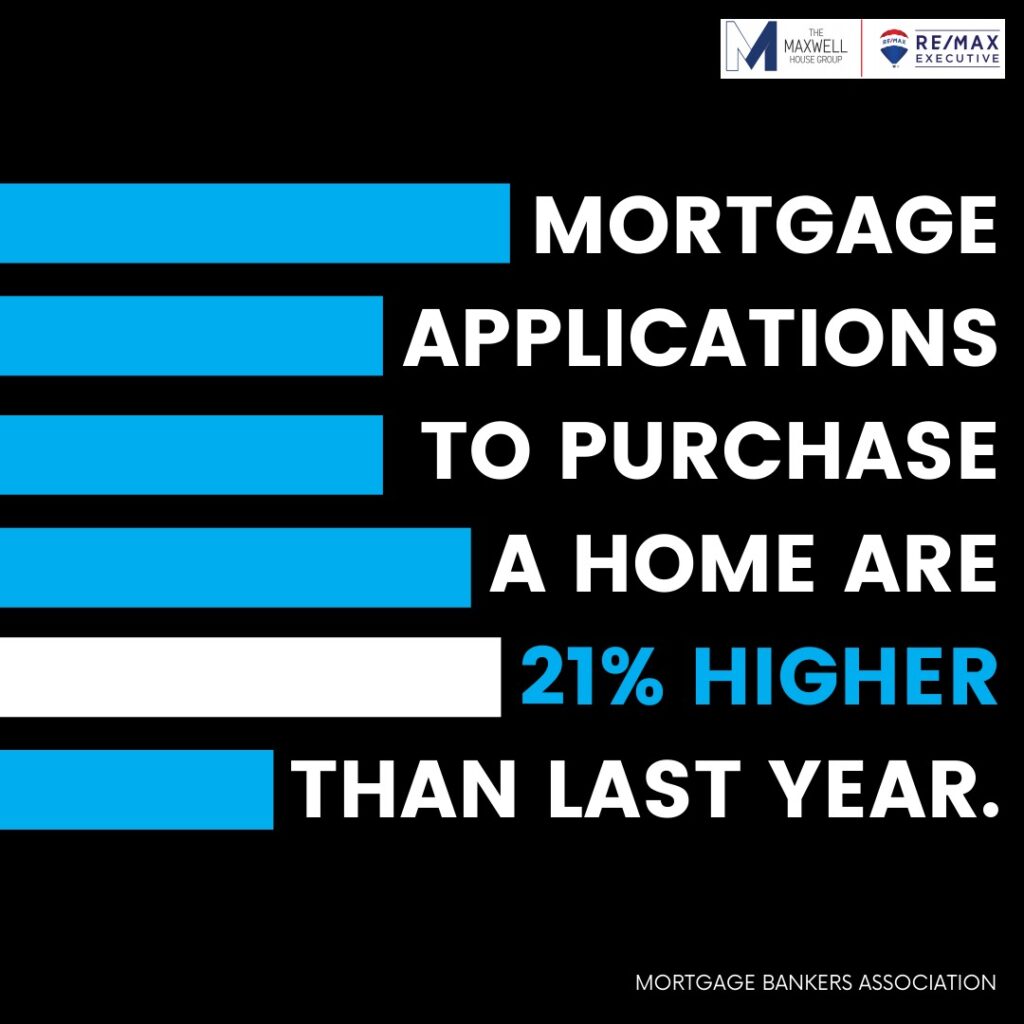

According to the Mortgage Bankers Association, applications for mortgages over $766,000 increased 59% year-over-year in Q3, the largest uptick of all price segments. In comparison, mortgages from $150,000 to $300,000 increased only 13% in comparison. One reason for the lower increase in the lower end price range could very well be due to scarcity of homes in that range.

Realtor.com just released their November Monthly Housing Market Trends Report. It explains:

“Nationally, the inventory of homes for sale decreased 39.2% over the past year in November…This amounted to 490,000 fewer homes for sale compared to November of last year.”

Right now, buyers are being cautious but, the fact remains, they are out in force. The desire for homeownership is still alive and well! With a vaccine on the horizon, more homeowners will be putting their houses on the market. This will better balance supply with demand and slow the rapid appreciation.

As a result of the expected increase in inventory, major organizations in the housing industry are calling for much more moderate home appreciation next year. Here are the most recent forecasts for 2021:

- National Association of Realtors: 4.5%

- Freddie Mac: 2.6%

- Fannie Mae: 2.1%

- Mortgage Bankers Association: 2%

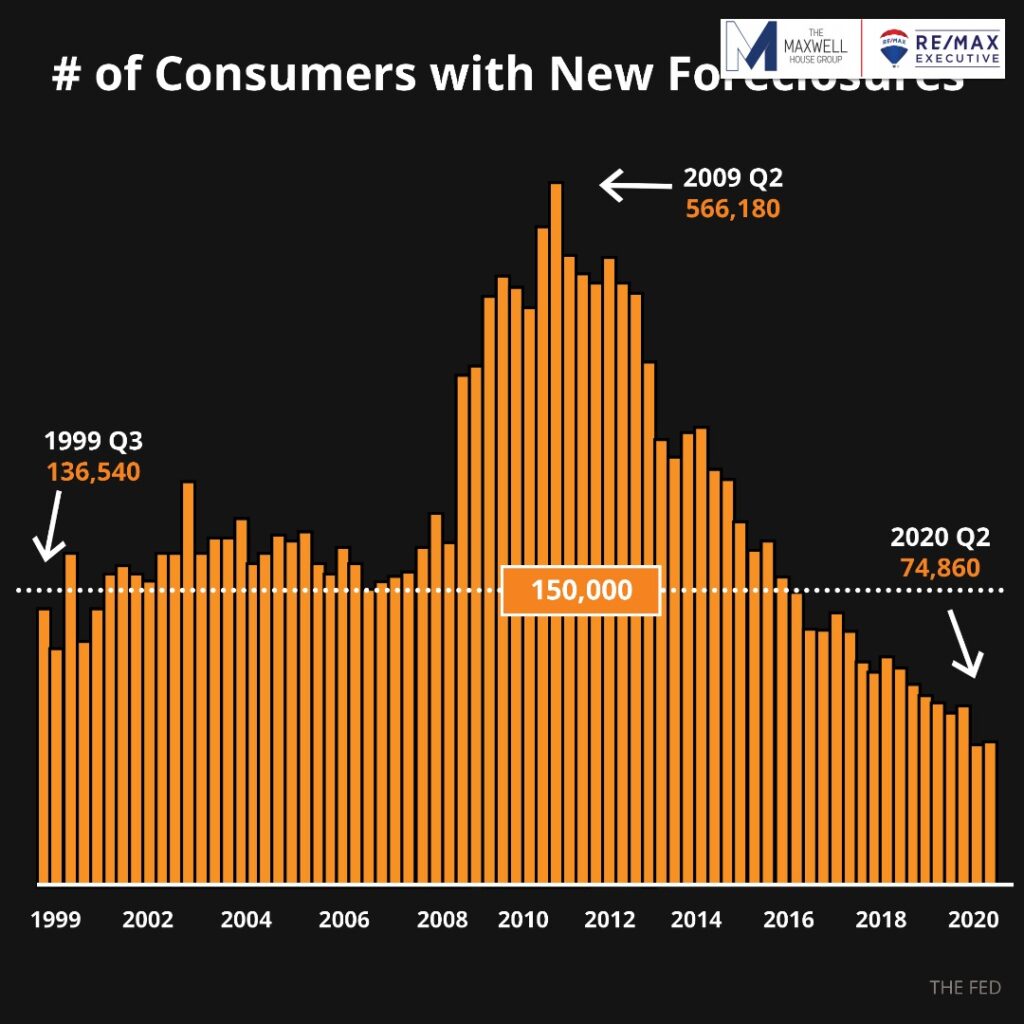

As well, the number of borrowers with active forbearances has declined over the past few months. According to HUD’s July 2020 “Neighborhood Watch” report, 17% of 8 million insured mortgages are now delinquent.

*Note that forbearances are also included in that 17% stat. As concerning as that may be, delinquency rates for subprime mortgages were much higher during the crash of 2008-2010. Ultimately real estate was at the CORE of The Great Recession whereas in 2020, it is more of a by-product.

With the easing of forbearances, expected increase in inventory and stabilizing market values, bubble theories can easily be dispelled.

Not sure about this market? Let’s talk! I’m happy to share data that is more tailored to your area, your neighborhood and your home. Call or text me at (704) 491-3310.

© Debe Maxwell | The Maxwell House Group | RE/MAX Executive | CharlotteBroker@icloud.com | Why talk of a housing bubble is blowing up!